IPTV – iTV through the backdoor?

|

The following article is taken from current study project “The advent of IP to TV” prepared for the School of Management and Information (SMI) at Steinbeis Hochschule Berlin by Nikolaus Reinelt, Master candidate Media MBA, Class of 2005. See here for TOC, study paper partly available on request. |

Taken a long term perspective, it is most likely that [IPTV and its] nascent closed and managed networks establish on the market. Bundled Triple Play offerings will fill up customer bases of IPTV providers and lock them into prepared service packages. Main competitive advantages for IPTV providers in this scenario stem from their Walled Gardens capability of ‘one face to the customer’ billing relation and their lean back product shaping. For telcos and cablers this implies also the saving from the decline in revenues of traditional core businesses. In best case even new customers will be attracted. Cablers and other access providers have to catch up (or, in some markets, take care not to fall back) with their own service bundles and work fiercely on the deployment of interactive enhancements of their offerings if they want to stay up-to-date with the interactive scalability of IP enabled platforms.

A core driver on open systems and broadband TV will be Microsoft. The Media Center has captured a key position in their end-consumer strategy, meaning that it will be marketed strongly, not only in terms of its TV features, but also as a one-stop entertainment device. Issues of intercompabilty and interface design will determine acceptance and herefore intensity of market pull for PC oriented solutions. X-Box and Playstation will have another stake in the embrace of business models for the reconfigured media environment by finding their particular role in the comfort zones, either outranking or complementing other solutions.

Decision makers in their projections should always be aware that the attention span of customers is not endless and after having decided for one or two services, the consideration set already will be fairly well-served. The economies of attention require value capture to be understood as a function of attention scarcity. Companies will prosper, if they can realize scale and scope effects in production or distribution for an efficient allocation of the scarce attention.

For a start, in the era of participation, new media will co-exist with old. It is indeed already increasingly hard to tell when one becomes the other. True, ever more people will upload short video clips to one of the many content aggregators or contribute in peer production activities. But that is not going to substitute the creative wizardry of a Steven Spielberg or the journalistic competence and value of the BBC’s great network of reporters. Instead microchunked media will offer many possibilities for differentiation of content providers and platforms At the same time it will be contributing to the disruption of wide parts of the media landscape. Especially when hurdles for accessing broadband connected PCs will be diminished and new platforms to control value capture will emerge. As we move from broadcast model to narrowcast (or multicast and point-to-point) many interactive services or business models have to be tried out.

It is just rational that broadcasters in this shift follow a bimodal strategy. Providing contents for fluid media experiences on disparate channels is part of the larger strategic adjusting to the afore mentioned intermediary role. Cooperating with gatekeepers of the new distribution hubs (IPTV providers, payTV operators or internet start-ups), they are placing an open bet on the various modes for incorporating the audience, no matter what happens. At least they will gain time to adapt their processes and structures before the next level of convergence between PCs and televised entertainment is reached.

The difference in the advent of IP to TV compared to the days of yore of interactive television is that now, driven by technical progress and convergence, core businesses of market players are being threatened and consumer behavior has evolved in a larger context to more individualization and fragmentation. Penetration of the internet and its undisputed benefits accelerated learning and strengthened demand for true interactive services.

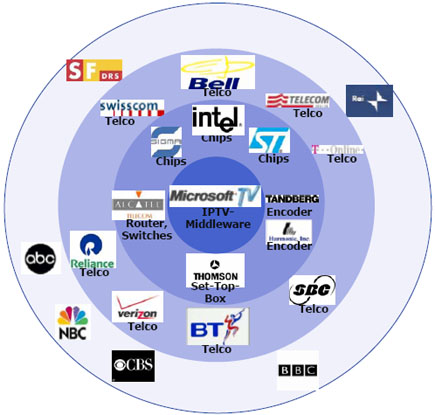

All trends listed in this paper already imply inherently most assets of the broad interactive television term: On-demand content, user interaction on backchannel, Walled Garden services, EPGs and others. IPTV can thereby under many aspects clearly be considered as interactive Television. Taken the fact that iTV is an umbrella term for any form of interactivity involved with television sets, it does not surprise that there are more than 50 definitions attached to iTV and nearby topics. The view held here is that true interactive television puts needs of viewers for interaction through an enhanced television experience in the middle. An interaction that is executed by an integrated backchannel. Interactive television over IP is, due to its disruptive nature and its technical proximity to the internet, a promising approach to solve the situation between broadcasters/distributors/CE-manufacturers that paralyzed many markets for a long time.

IPTV is as such interactive TV although not through the backdoor – it will be coming to homes right next to its own backchannel.